The Middleman Tax on Every Film You Love

- May 15

- 11 min read

Modern filmmaking has quietly become an industry that pays almost everyone — except the people who actually make the film. Here is the data, layer by layer, and the case for tearing the layers out.

There is a strange paradox at the centre of the entertainment economy. The person who has the idea, the artist who animates the frame, the composer who writes the theme, the VFX house that conjures the impossible — these are the people who create the value an audience actually pays for. And these are, with remarkable consistency, the people who capture the least of it.

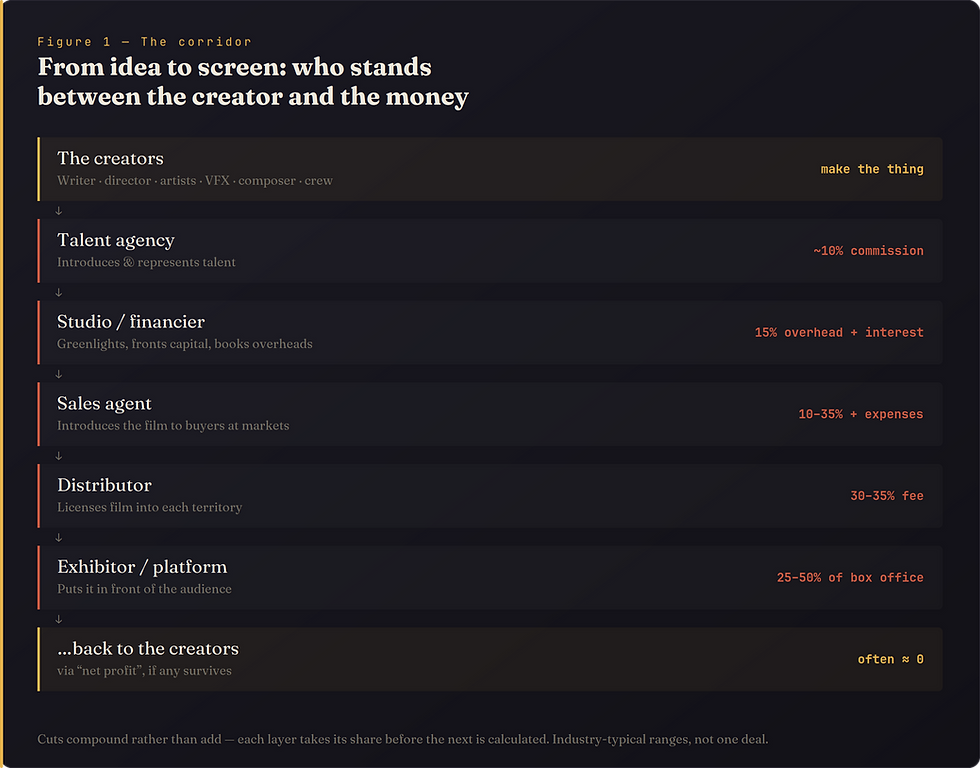

Between the spark of an idea and the light hitting a screen sits a long corridor of intermediaries. Agents introducing talent to producers. Sales agents introducing films to distributors. Distributors introducing films to exhibitors. Aggregators, packagers, brokers, "market representatives," and the people who introduce the people. Each one provides a real-sounding service. Each one takes a cut. And by the time the money has finished its journey back down the corridor, the cupboard the creators are standing in front of is very nearly bare.

This is not a moral complaint. It is an arithmetic one. The argument of this piece is simple and, we hope, hard to dismiss: the structure of the film business systematically over-rewards intermediation and under-rewards creation — and that this is now a solvable problem, because the original reasons those middlemen existed have been overtaken by technology.

It is worth being fair to history first. Markets, agents and distributors did not appear out of greed. They appeared because, for most of cinema's existence, there was no other way to solve four genuinely hard problems: discovery (how does a buyer in Seoul learn your film exists?), trust (how do two strangers transact across a continent?), financing (who fronts the money before a frame is shot?) and risk (who absorbs the loss if it flops?). Middlemen were the technology of their time for solving coordination. The question this piece asks is whether that technology has now been superseded — the way travel agents, stockbrokers and classified-ad sellers were superseded — by platforms that can do discovery, trust and matching at a fraction of the cost, and in the open.

Exhibit A — The Accounting: how a $475 million hit can earn "nothing"

Start at the end of the corridor, with the most studied trick in the business: so-called Hollywood accounting. The mechanism is mundane. A studio sets up a film as its own little company, then bills that company for services the studio itself provides — distribution, marketing, overhead, interest on the money it advanced. Industry analyses put the studio's distribution fee at roughly 30–35% off the top of everything the film earns, with a further ~15% production overhead and ~10% marketing overhead layered on, often before the film is even allowed to show a rupee of profit.

The consequence is that "net profit" becomes a number that, by design, almost never arrives. Industry estimates suggest only about 5% of films ever officially report a net profit. Anyone paid in net points is holding what insiders bluntly nickname "monkey points" — a share of a number engineered to stay at zero. The famous casualties are not obscure flops:

Return of the Jedi earned around $475 million on a roughly $32 million budget and was reported to have "never gone into profit" — which is how the actor inside the Darth Vader suit was told his profit share did not exist. Forrest Gump grossed over $600 million and was booked as a roughly $62 million loss. Instalments of the billion-dollar Lord of the Rings and Harry Potter franchises were reported unprofitable too; Peter Jackson sued his studio over the accounting. The films made money. The audience knows they made money. The ledger, routed through shell companies, says otherwise — and "net profit" participants are paid on the ledger.

Exhibit B — The Representation: when your own agent earns more if you earn less

Move one step up the corridor, to the people meant to be on the creator's side: the agents. For decades, the largest talent agencies did not simply take the traditional 10% commission on what their clients earned. On packaged projects they collected a "packaging fee" paid directly by the studio — commonly structured as the so-called 3-3-10: a slice of the licence fee up front, a slice deferred, and a slice of the back-end profits.

Read that structure again, because it contains the rot. When an agency is paid out of the studio's pocket from the project's profits, every rupee paid to the writer reduces the pool the agency draws from. The agent — the one person legally meant to maximise the client's compensation — now makes more money when the client makes less. The Writers Guild of America called it a structural breach of fiduciary duty. In April 2019 it told its members to do the unthinkable: more than 7,000 writers fired their own agents. The standoff lasted over a thousand days. Only after the four dominant agencies — who between them accounted for more than 90% of packaging deals — signed on did the practice end, with commissions returned to a flat percentage of what the writer actually earns.

"Our agents are our fiduciaries — every dollar they make should be a percentage of the dollars we make." — the principle at the heart of the WGA's packaging-fee campaign

It took a 1,000-day labour war to restore a principle that should be obvious: the people who connect you to work should be paid as a share of your success, transparently, and not by the counterparty across the table.

Exhibit C — The Market: the toll booth between a finished film and a buyer

Now the part of the corridor most invisible to audiences. A finished independent film cannot simply walk up to distributors around the world. It is taken to a sales agent, who carries it to the great trade fairs of the business — the Marché du Film at Cannes, the American Film Market, the European Film Market in Berlin. These are extraordinary engines of connection: the Cannes market alone draws on the order of 12,500 professionals presenting roughly 4,000 films and projects, with reported turnover running into hundreds of millions of dollars.

For that introduction the sales agent takes a commission — quoted anywhere from 10% to 35% depending on who you ask — plus recoupable expenses typically capped around $50,000–$75,000 for travel, screeners and marketing materials. Crucially, this comes off the top, before money reaches the production. One industry breakdown shows the texture: on a modest indie with $3 million in international minimum guarantees, a 12% commission and $60,000 of expenses already shave the producer's take down to roughly $2.58 million — and that is before the distributor's and exhibitor's cuts further down the line have even begun.

Exhibit D — The Artists: they built the spectacle, then went bankrupt building it

If you want a single, undeniable image of value flowing away from its creators, it happened on live television in February 2013. The visual-effects studio Rhythm & Hues had conjured the tiger and the ocean of Life of Pi — work so good it won the Academy Award for Best Visual Effects. Eleven days before the ceremony, the company filed for bankruptcy. As its supervisor began, on stage, to speak about the crisis engulfing his industry, his microphone was cut and the orchestra played him off with the theme from Jaws. Outside the theatre, some 400-plus VFX artists were protesting in the street.

This was not a freak event. Between 2003 and 2013, roughly 21 VFX houses closed or went bankrupt. Rhythm & Hues had employed more than 700 people at its peak; it laid off around 250 of them, many by phone on a Sunday night. The cause was structural, and it rhymes with everything above: VFX houses bid fixed prices on jobs, then absorb every cost overrun out of their own pockets, with almost no leverage against the studios who are their only real customers — all while chasing whichever country is dangling the biggest tax subsidy that year. The work dominates the modern box office. The people doing it cannot keep the lights on.

Exhibit E — The Black Box: the streaming era made the money invisible

For generations, the deal that kept working creators afloat between jobs was the residual — a payment each time their work was shown again. Streaming quietly broke it. Viewing data sits inside the platforms; the formulas that once tracked a rerun no longer map onto an algorithmic feed. The result is a new kind of opacity, where a creator cannot even see whether their work is being watched, let alone be paid fairly for it.

The human scale of this became a meme during the 2023 strikes, when an actor from a globally famous Netflix series shared a foreign-residual statement totalling about $27 — for roughly a decade of a hit show. At the macro scale, the picture is just as stark: total writer earnings fell from a record $1.89 billion in 2022 to about $1.29 billion in 2023 — a roughly $600 million drop — as the industry contracted and a months-long strike ground production to a halt. The fight, at its core, was a fight for transparency: pay us based on what people actually watch, and show us the numbers.

The Mirror at Home: the same corridor, in Indian cinema

None of this is a uniquely Hollywood disease, and it would be dishonest to pretend otherwise from Bengaluru. Indian film distribution is itself a layered system: the country is carved into roughly a dozen distribution circuits, and a producer typically sells territory rights to distributors — most often on a minimum-guarantee basis — who in turn negotiate with exhibitors. After the 2009 multiplex standoff, the exhibitor–distributor split was set on a sliding scale that starts near 50:50 in week one and shifts steadily toward the exhibitor — around 70:30 by the fourth week. The structure differs in its details; the shape is identical. Value passes through many hands, each of which is set up before the people who made the film see a paisa.

The Counterpoint: proof that a single, honest cut works (no middleman)

Here is the optimistic half of the argument. Look at the creator economy and you see the same value chain compressed into one intermediary instead of a dozen. On YouTube's long-form program, the platform keeps 45% and the creator keeps 55% — a single, published, predictable split. There is no agent taking 10% of that, no sales agent taking another 15%, no distributor taking 30%, no shell company quietly absorbing the rest. The creator can see their views and their revenue in close to real time.

We should be honest about the limits — staying logical matters more than scoring points. The creator economy is not a utopia: the platform still sets the split, still controls payout timing, and take rates across platforms run anywhere from 20% to 45%. But the contrast with mainstream film is the entire lesson. A creator on a platform loses a knowable fraction to one party, in the open. A filmmaker in the traditional system loses an unknowable fraction to many parties, in the dark. One model is merely expensive. The other is structurally opaque.

The Cost to the Art: why this also produces worse films

There is a second cost beyond the money, and it is the one that should worry audiences most. When every project must pass through the same narrow set of gatekeepers, the question those gatekeepers ask is not "is this a great story?" but "is this a safe business decision?" A small number of people in a small number of rooms decide which ideas get to exist — and they are, rationally, optimising for downside risk, not for wonder. The corridor does not merely tax creativity. It filters it, and the filter is tuned to the familiar.

This is why so much of what reaches us feels engineered rather than authored. The passion for telling a great story competes, at every gate, with the incentive to extract a margin from the introduction. Strip the corridor down, and the question can change back to the one that built cinema in the first place.

"We believe the next wave of great cinema will not be decided in boardrooms but co-created by communities, powered by technology, and guided by data-backed market signals." — Movie Colab

The Alternative: rebuild the corridor as a trust layer, not a toll road

Return to those four problems middlemen originally solved — discovery, trust, financing and risk. The reason a sales agent could charge for an introduction is that, historically, there was no neutral place where a producer in Mumbai and a buyer in Berlin could find each other, verify each other, and transact with confidence. Trust had to be brokered because it could not be infrastructure.

That is precisely the assumption a platform can overturn. Movie Colab is being built as a single connected system that runs a project from the first draft to final delivery — and in doing so, it can carry the very functions that justified the middlemen, at near-zero marginal cost and in full view of everyone involved. Matching can be a search, not a favour. Reputation can be a verifiable track record, not a phone call. Contribution can be logged frame by frame, so that when value is shared, there is no shell company between the work and the wallet.

It is one suite, designed so every role, file and task flows through the same pipeline — which is also the only honest way to make the money flow legible:

Script Viz — turns the script into a living visual plan, keeping authorship at the centre from the very first stage.

Table Read — brings the story to life early, so a great idea proves itself on its merits, not in a boardroom.

Projects — the connected production hub: tasks, versioning, frame-accurate reviews, so contribution is visible and traceable.

Sync Space — real-time collaboration that lets distributed teams work as one, without a layer of coordinators in between.

Artist Hub — a direct, global network of artists and production experts: discovery and matching without the broker's cut.

Movie Colab VR — virtual production that collapses cost and distance, putting more of the budget back into the craft.

This is not a promise to abolish distribution overnight, and we won't pretend it is. It is something more durable: the patient construction of the rails on which a fairer model can run. Every film already coordinated through one transparent pipeline is one film whose value can no longer disappear into the dark between the hands. The studios behind projects like Heart of Akhnar and Shoorveer did not just use a tool; they kept their project — and its record of who did what — in one place they could see.

The middleman is not a villain. He is a symptom of an old problem that finally has a new solution. Trust used to be expensive, so we paid people to broker it. Now trust can be built into the platform itself — and the people who make the film can, at last, keep the largest slice of the value they create.

Put the value back where it's made.

Sources & notes

Studio distribution fees (~30–35%), production overhead (~15%), marketing overhead (~10%) and the "~5% ever report net profit" estimate, plus the Return of the Jedi, Forrest Gump, Harry Potter and Lord of the Rings examples: HowStuffWorks and the Hollywood-accounting literature. Agency packaging fees, the 3-3-10 structure, ~7,000 writers firing their agents and the 1,000-day campaign: Deadline, TheWrap and WGA materials. Sales-agent commissions (10–35%), expense caps ($50–75K) and the $3M worked example: Raindance, Vitrina and Guerrilla Rep. Marché du Film scale (~12,500 professionals, ~4,000 films): market reporting. Rhythm & Hues bankruptcy, the cut microphone, the 400+ artist protest and ~21 VFX closures (2003–2013): Deadline, The Hollywood Reporter, TheWrap and Life After Pi. Streaming residual collapse, the ~$27 statement and the $1.89B→$1.29B writer-earnings fall: Variety and Fortune, citing WGA data. Indian distribution circuits, the minimum-guarantee model and the post-2009 sliding exhibitor split: Indian industry explainers and contemporaneous reporting. Creator-economy splits (YouTube 55/45; 20–45% platform take rates): YouTube and creator-economy payment research. Figures are industry-typical ranges and illustrative composites, presented to show the shape of the value chain rather than the terms of any single deal.

Comments